Profit Does Not Equal Cash

As a CFO, I see a lot of business owners who think that net profit equals cash. Let me clear: it absolutely does not!

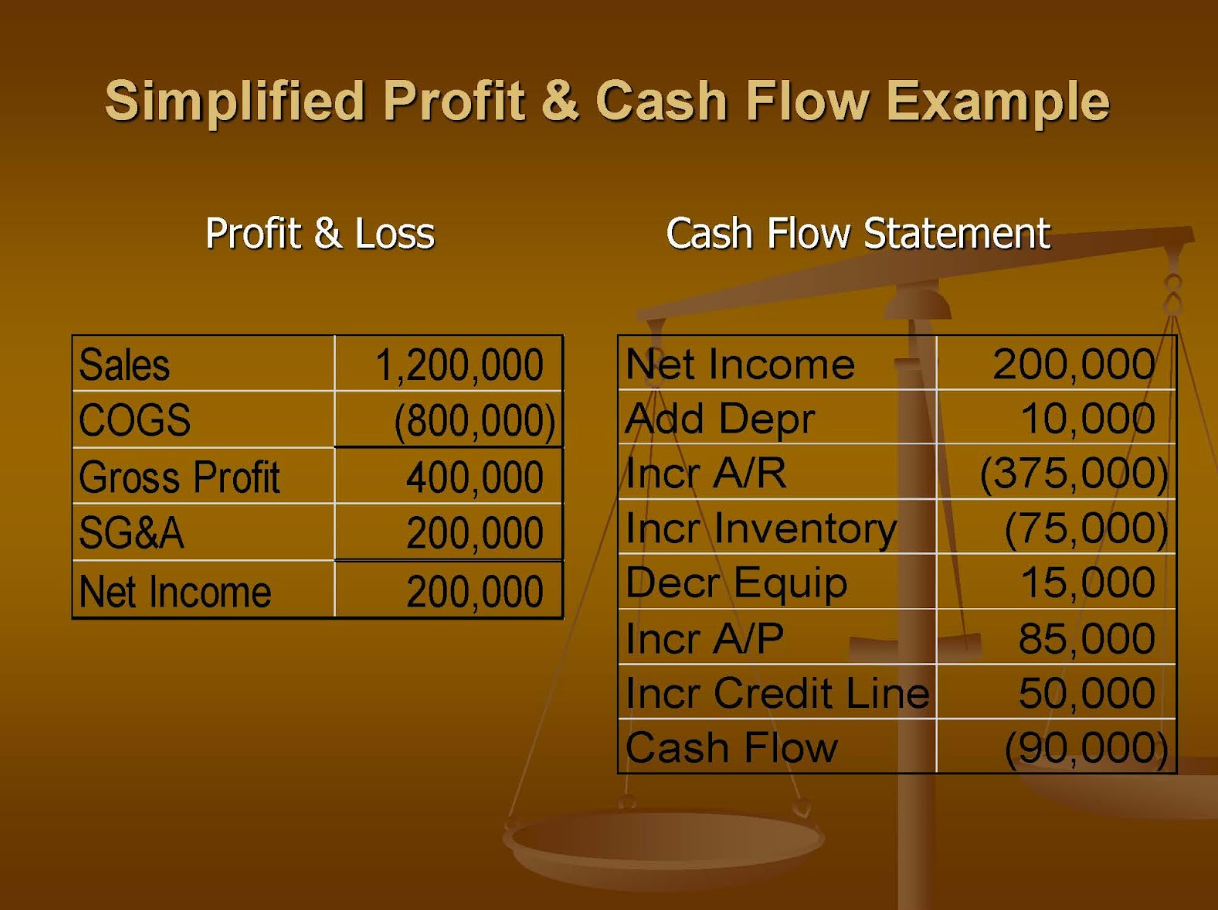

Business owners who watch their profit and loss statement regularly think they are also simultaneously watching their cash flow. Managing the P&L and managing cash flow are two separate and distinct functions. For example, let’s say you have a cost of goods sold of 800,000, leaving a gross profit of 400,000. Then when you deduct 200,000 for SG&A, which is selling general and administrative expenses, you are left with a net income of 200,000. That $200,000 net income is carried over to the cash flow statement. (See Illustration Below)

This cash flow statement starts out with net income, which as we learn from the P&L, is $200,000 and that is obviously a source of cash and reflects positively toward cash flow. Added to net income is a non-cash expense called depreciation, but this adjusted net income is not the whole cash story as is commonly thought by business owners because the very next line item shows an increase in accounts receivable when the change in accounts receivable balances increase.

This is a use of cash because money is being tied up in receivables. Now, on the other hand, it would be a source of cash if the change in accounts receivable came down because that means you worked down your receivables receiving more cash. In this example, the change in accounts receivable increased, causing a negative impact on cash flow. The next change in a balance sheet account that occurred is inventory. In this example, inventory increased. The increase of inventory is also a use of cash if you're purchasing more inventory using cash and therefore has a negative impact on cash flow. The next line item is a decrease in equipment. This indicates that equipment was probably sold well when you sell equipment and get the cash, that would represent a source of cash and therefore a positive impact on cash flow. The next line item is an increase in accounts payable. An increase in accounts payable indicates that you're delaying payments to the trade and that's also a source of cash because you're not giving it to the trade, you're keeping it. The final line item in this example is an increase in the line of credit, which is an obvious source of cash because you're taking money from a line of credit at the bank and putting it in your company bank account.

Although this company made a $200,000 net profit, the company lost cash in this particular year. Upon a quick analysis of this cash flow statement, the cash tied up in accounts receivable was probably the impetus that led to the cash reduction.

As you can see, a business owner who only looks at the P&L will make bad business decisions.